After eight years of growth, the market still is thriving. Further, most firms believe it will continue to improve through the end of 2018 and have backlogs to prove it. But some firms are beginning to become wary about what 2019 will bring, both for the market and the economy as a whole.

After eight years of growth, the market still is thriving. Further, most firms believe it will continue to improve through the end of 2018 and have backlogs to prove it. But some firms are beginning to become wary about what 2019 will bring, both for the market and the economy as a whole.

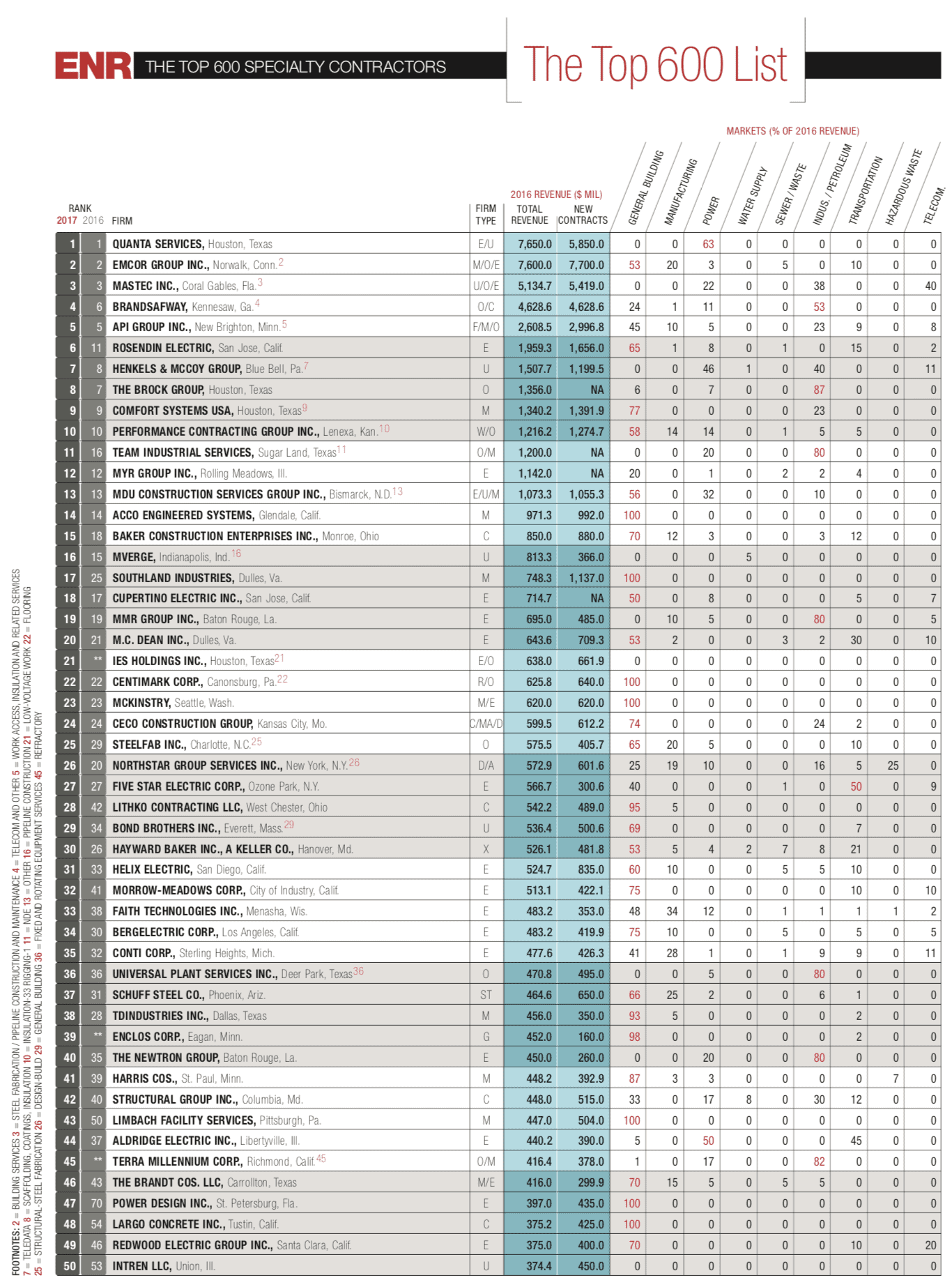

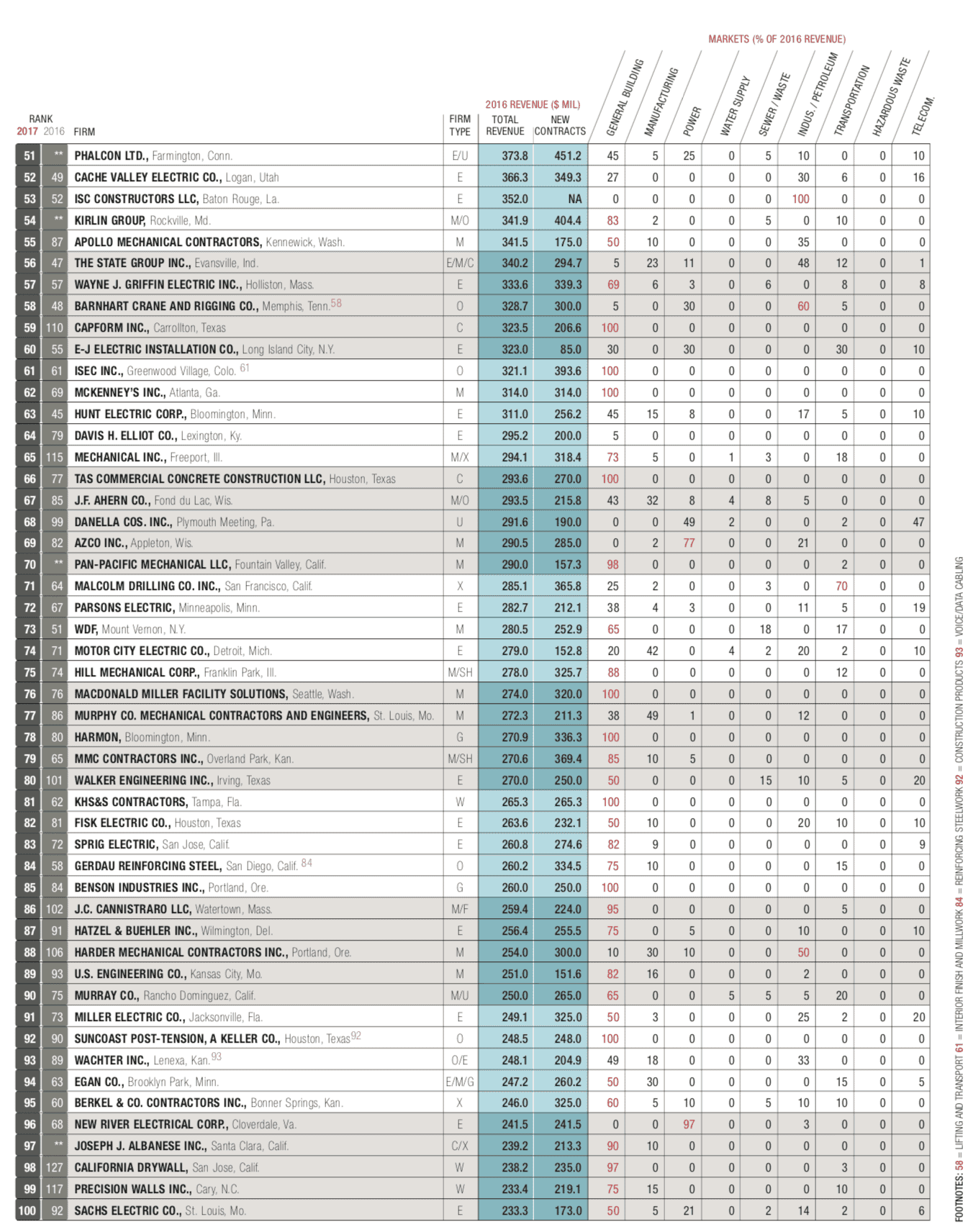

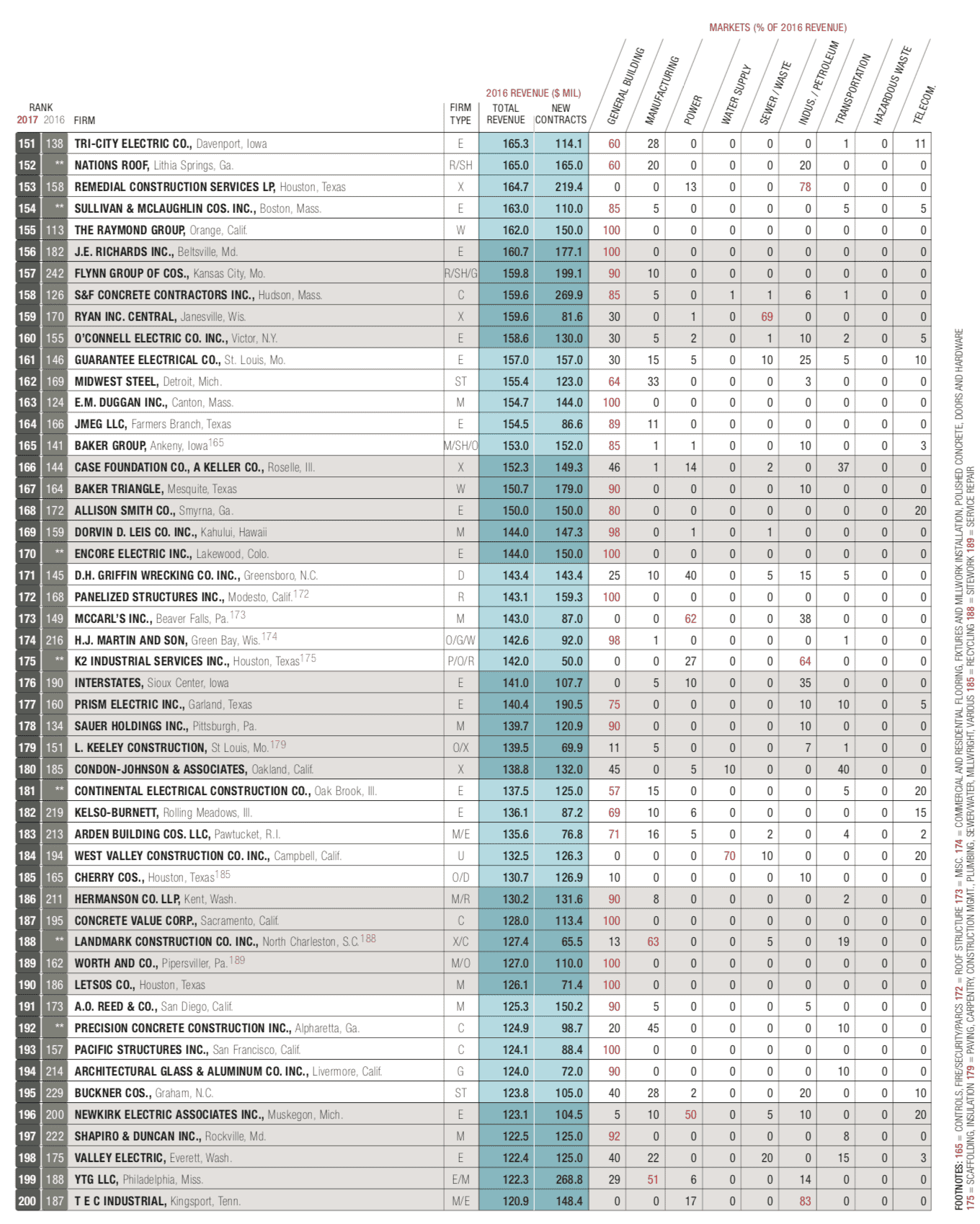

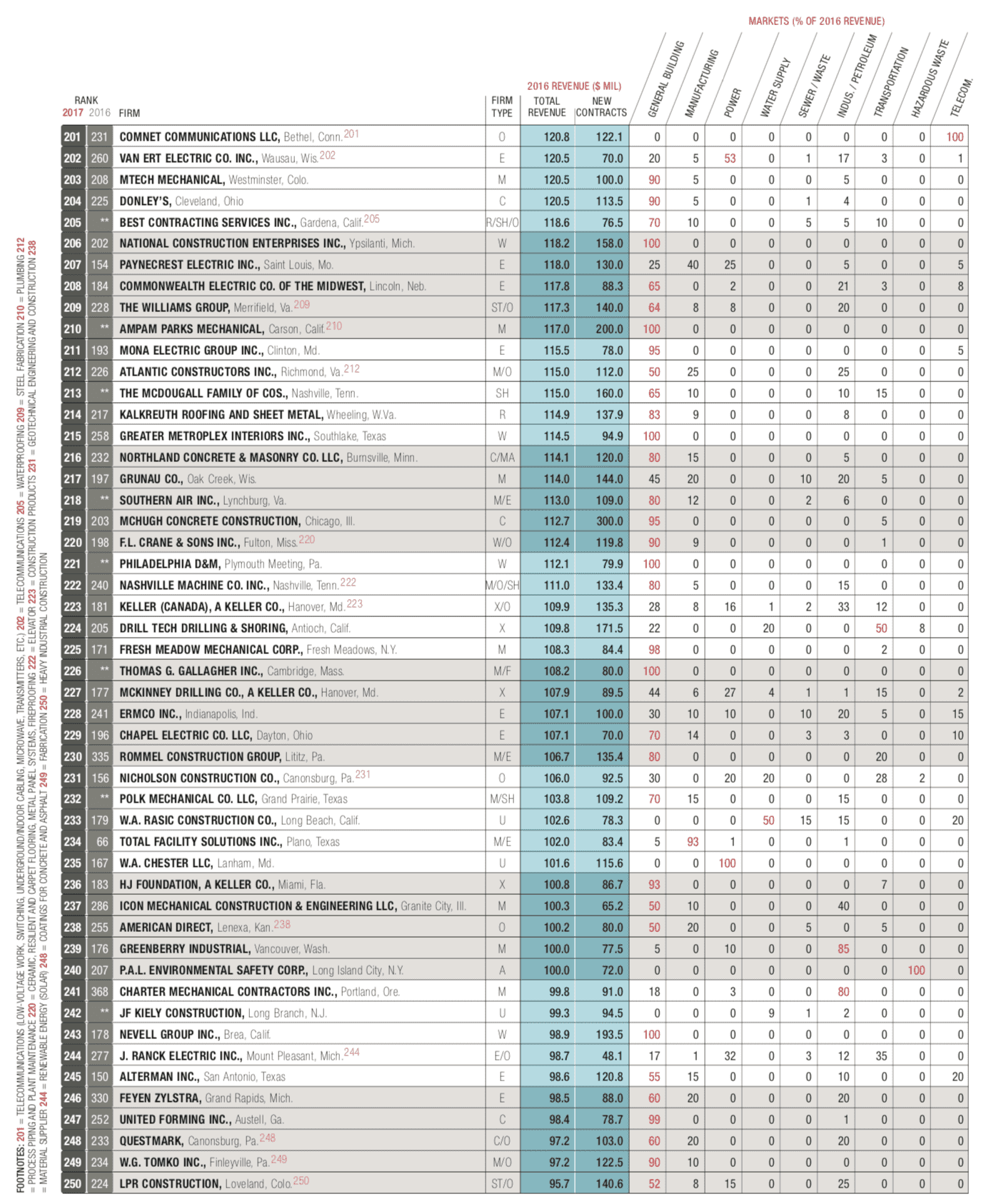

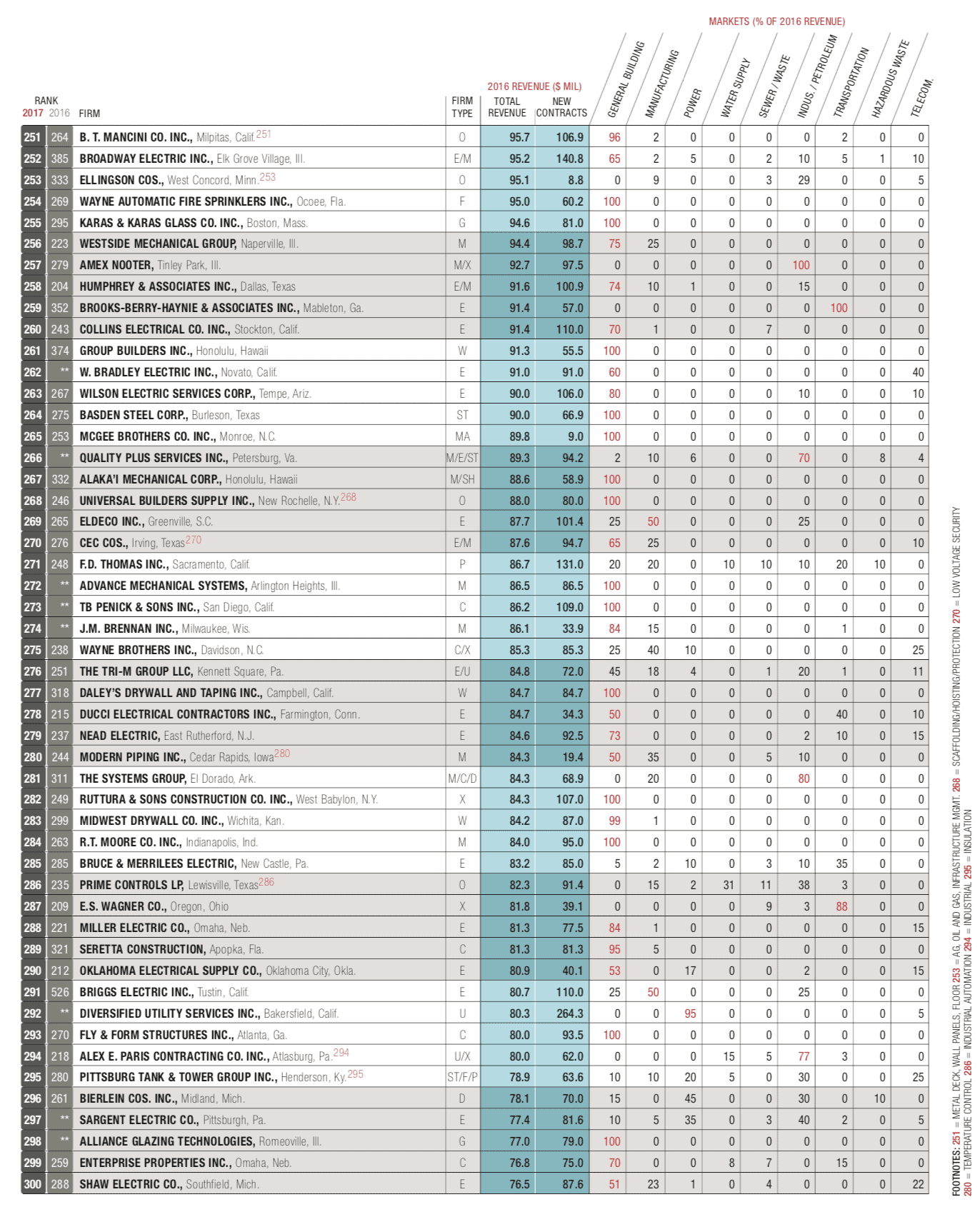

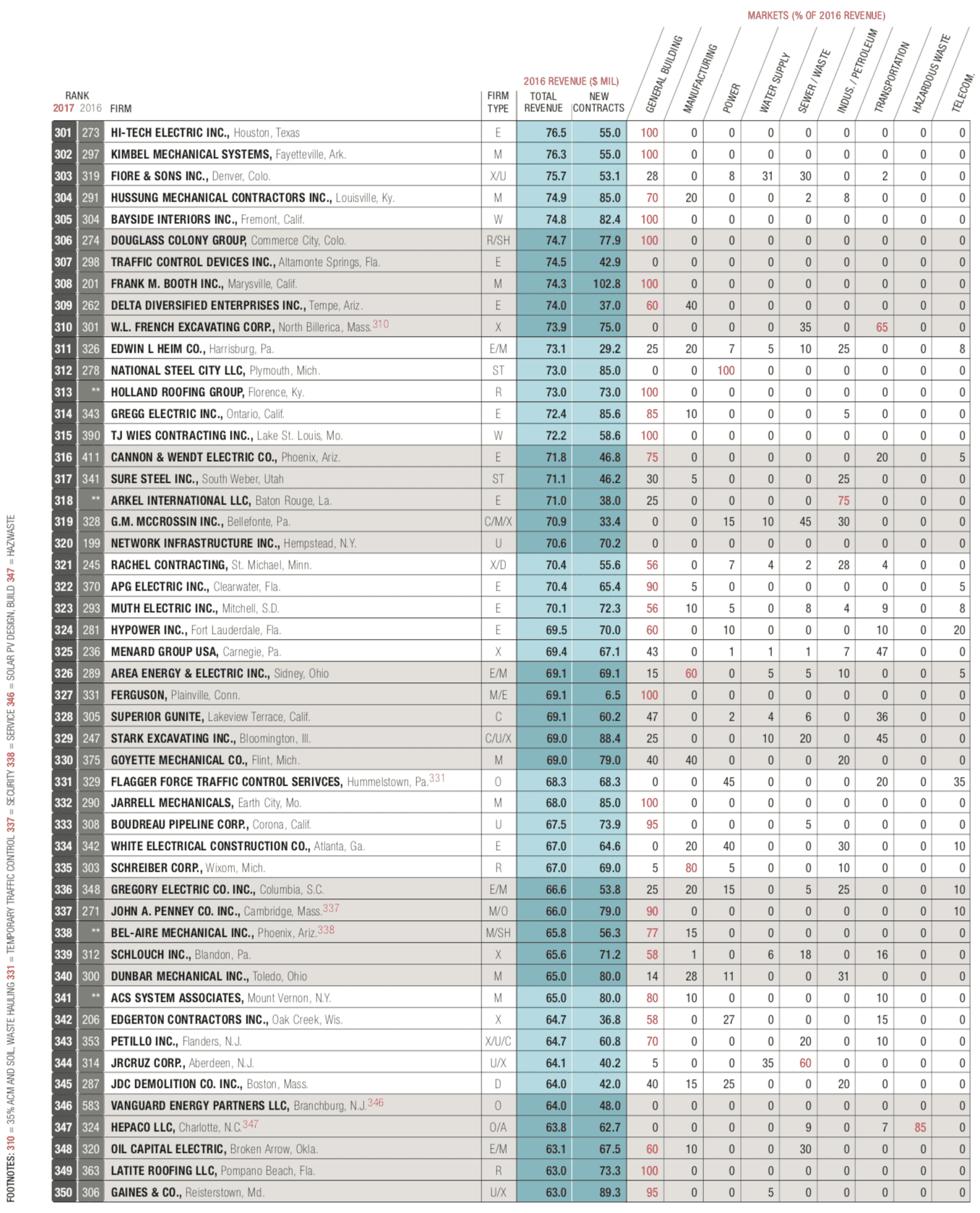

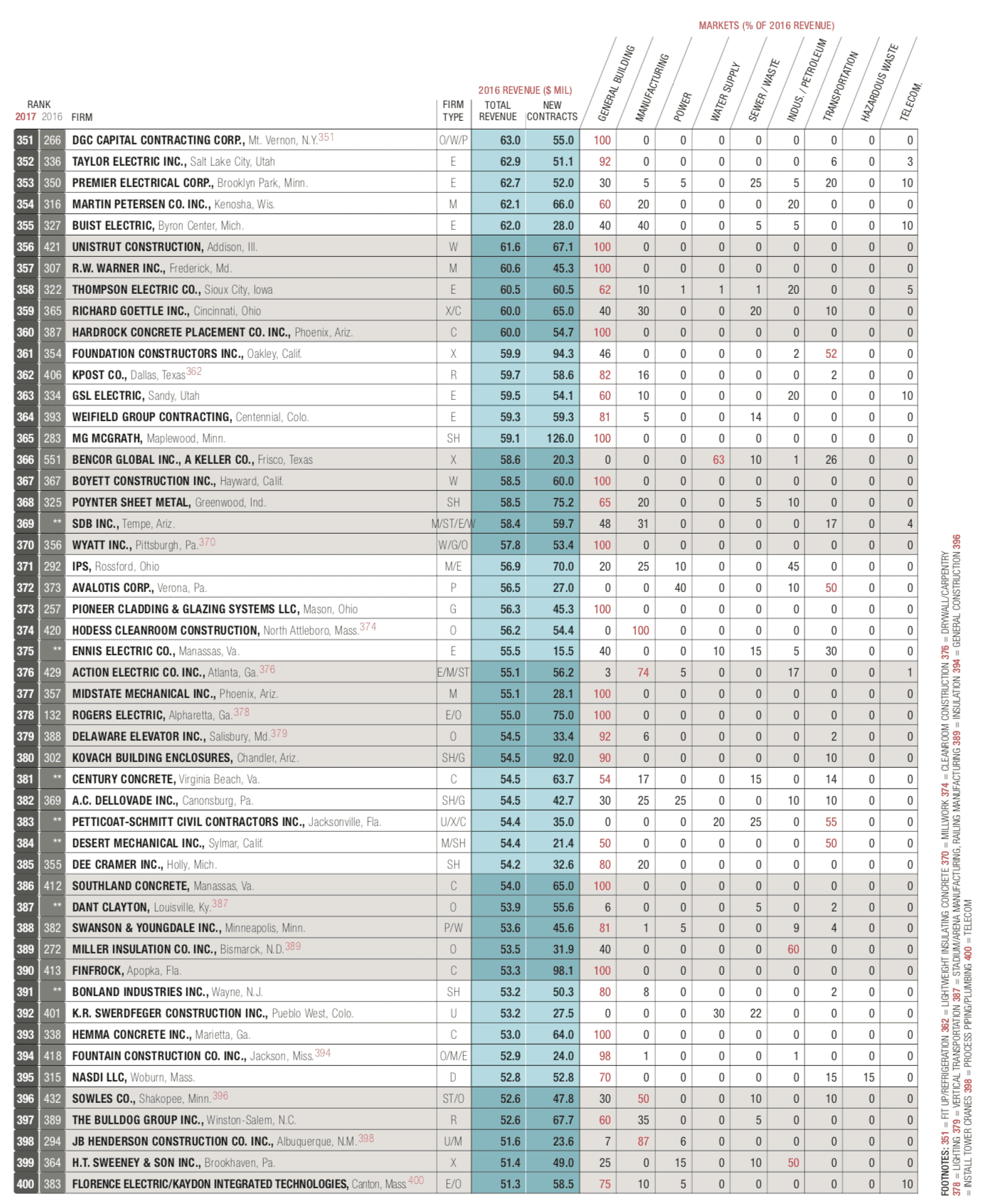

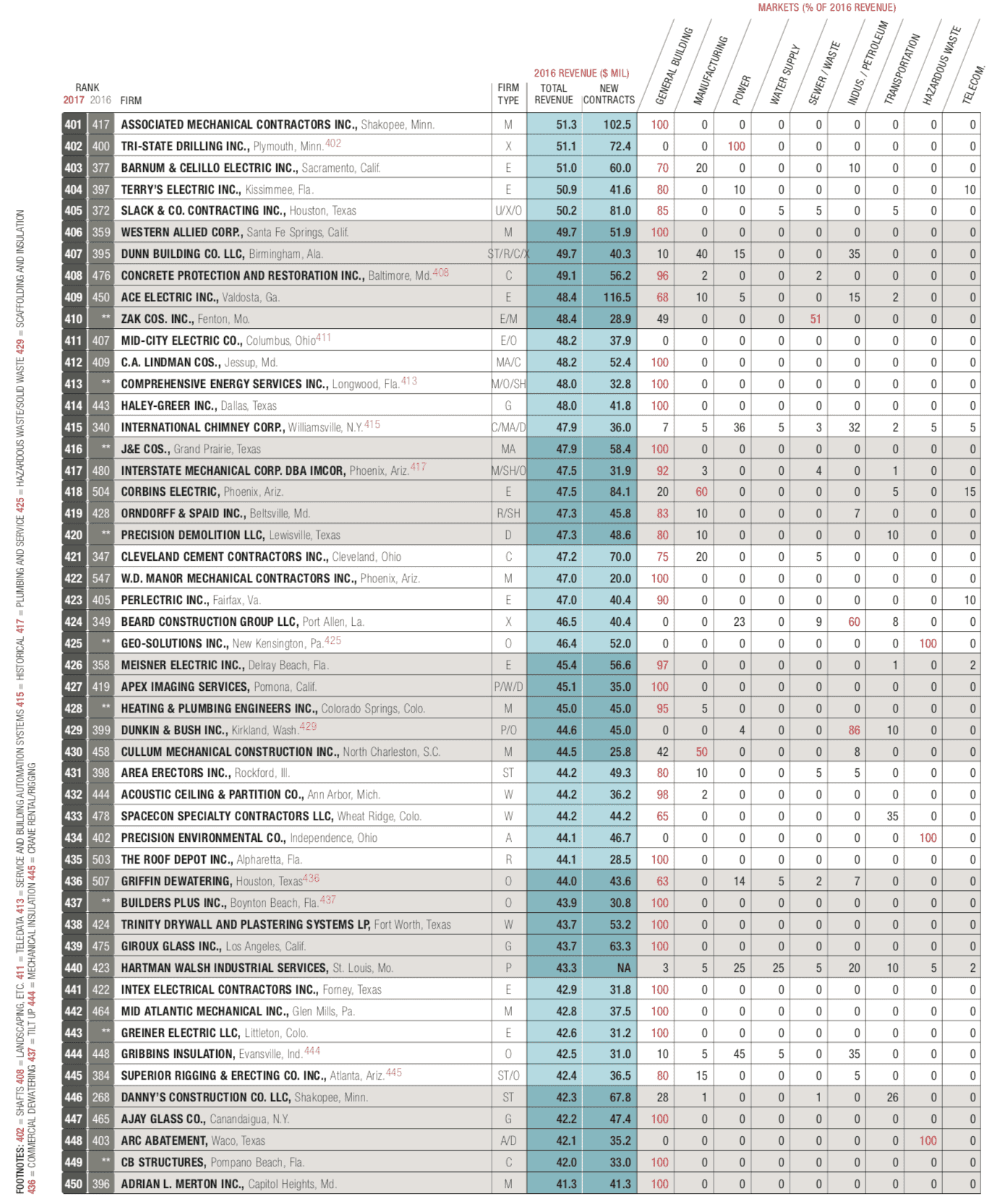

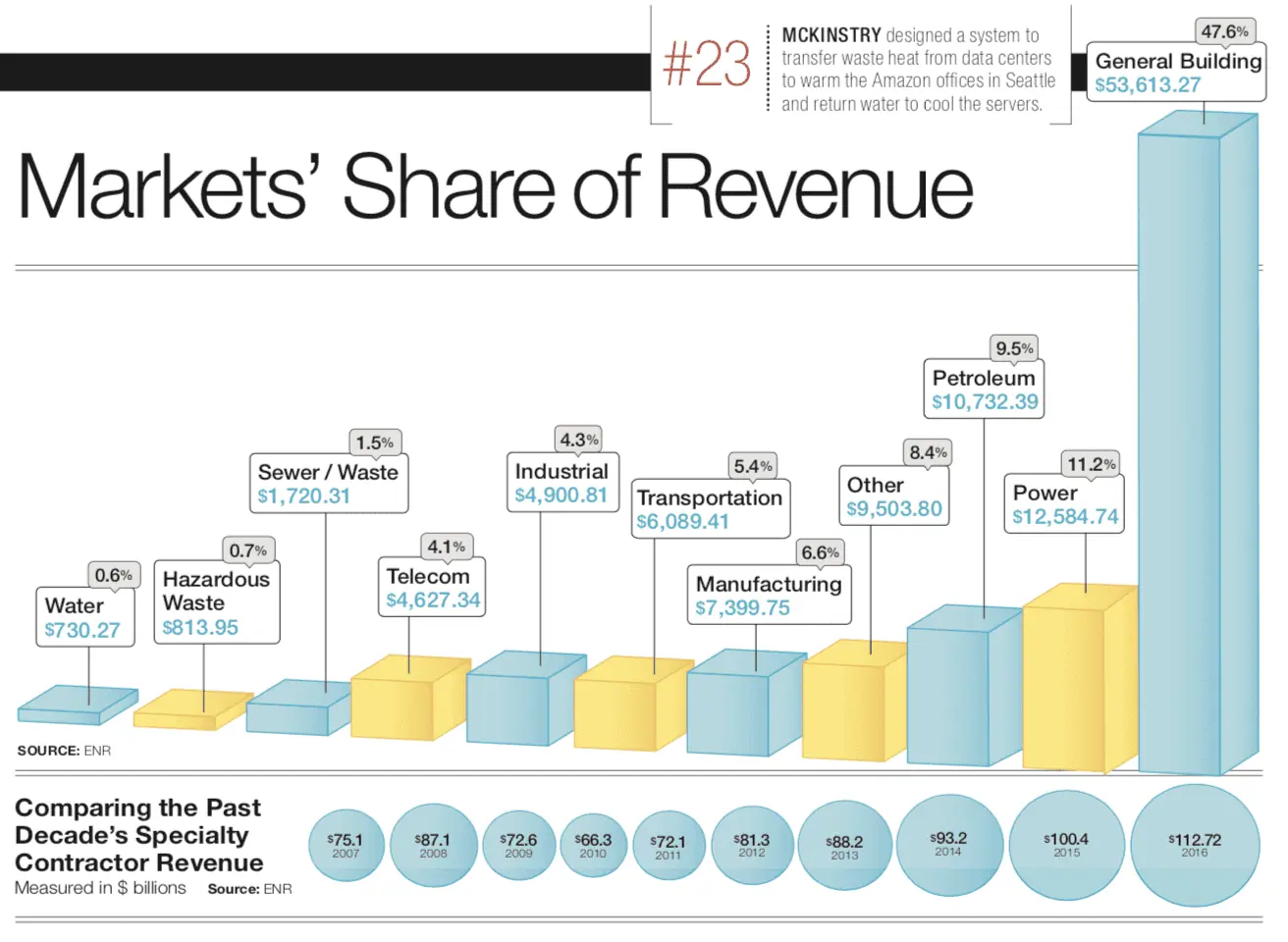

The impressive strength of the market can be seen in the results of this year’s ENR Top 600 Specialty Contractors list. As a group, the Top 600 cleared revenue of $112.72 billion in 2016, up an impressive 12.2%, from $100.43 billion, in 2015. Further, many Top 600 leaders think the recovery still has steam in it.

Many contractors are enthusiastic about the current and future market. “We are seeing tremendous growth year-on-year and have a record backlog,” says Charles Bacon, CEO of Limbach Facility Services. He says Limbach currently is tracking $3.1 billion in opportunities, up from $2.4 billion at this time last year. “I don’t see a recession any time soon,” he adds.

One good sign of the expanding market is that backlogs are growing. The Washington, D.C.-based Associated Builders and Contractors’ Construction Backlog Indicator, which measures the average length of backlogs among all its contractor members, rose to nine months during the first quarter of 2017, up 8.1% from the fourth quarter of 2016, says Chuck Goodrich, president of Gaylor Electric Inc. and 2017 ABC chairman. “For the first time in the series’ history, every category—firm size, industry and region—registered quarterly growth in CBI. CBI is up by 0.4 months, or 4%, on a year-over-year basis,” he says.

Many market sectors look very good. “There is a significant need to build new and maintain existing electric power and oil-and-gas infrastructure throughout North America. As a result, our customers’ multiyear capital programs and projects are larger and more complex than they have ever been,” says Duke Austin, CEO of Quanta Services.

The long-term prospects in energy markets seem strong. “Power plants are changing sources of energy, and that means the power market should be strong for the next 15 years,” says Anthony Guzzi, CEO of Emcor Group. The domestic oil market also should continue to grow, he predicts.

On the buildings side, most contractors are optimistic. “Health care and manufacturing continue a steady growth. The emergence of internet-based retail sales has increased our focus on distribution and data-center construction,” says Goodrich. “We have seen an increased demand in the mission-critical health-care and transportation markets, while commercial and residential markets have held steady. Our pipeline for

the next 12 to 24 months looks very healthy,” adds Brian Brobst, marketing director for Rosendin Electric.

Storm Clouds Forming?

Storm Clouds Forming?

Storm Clouds Forming?

Storm Clouds Forming?However, there are many who see storm clouds on the horizon. “I am hearing more contractors talking about the potential for a recession coming up in the next 12 to 18 months,” says E. Colette Nelson, chief advocacy of cer for the American Subcontractors Association, Alexandria, Va. She says many contractors don’t believe the market will drop off in the foreseeable future, but she cautions contractors should prepare just in case.

Nelson is not the only one who is concerned about long-term markets. “National construction market forecasts predict a slowdown in 2018 due to general concerns about a sluggish U.S. economy.” says Marc Paolicelli, chief customer of cer at RK Mechanical Inc.

Many contractors are preparing in case of a downturn. “Earlier this year, we felt a need to be prepared in case markets slowed later in 2018 or into 2019,” says Brad Wucherpfennig, president of Baker Concrete Construction. “However, so far, the volume of work appears to be fairly steady.”

Generally, contractors predict this surge will be maintained through 2018 and into 2019. “ we believe that building a strategically intelligent backlog of business is paramount in the ability to successfully thrive and survive the inevitable changes in our market place,” says Skip Mancini, president of B.T. Mancini Co.

One of the difficulties in a market this strong is that many contractors are tempted to expand by pursuing larger projects, which can cause problems. “We have invested heavily in training, safety and technology because that is what customers demand,” says Guzzi. He says firms that chase work into high-end markets may run into problems coping with these demands. “It is a tough time for small and midsize contractors trying to do bigger jobs than they are used to,” he observes.

Guzzi says contractors have to be especially careful in such a strong market. “You can’t take jobs that you can’t staff, and you have to be careful who you team with and how clearly de ned the scope of work is,” he says. “Contractors that chase work just to add volume will be the rst ones to get into trouble.”

Mergers and Acquisitions

Mergers and acquisitions continue to have an impact on the specialty-contractor market. The recent merger between Brand Energy & Infrastructure and Safway Group was the biggest on the list, becoming the $4.6-billion industrial services giant BrandSafway.

Another major acquisition last year was Emcor Groups’ purchase of Ardent Services, a $250-million electrical contractor in the industrial section. Guzzi says Emcor continues to look for the right firms to acquire. He adds, “We are looking for solid firms … preferably in the $100-million to $150-million range.”

Many in the industry say the M&A trend will start to accelerate. “It seems as if there is a high concentration of baby boomers. As these individuals transition out of their businesses, there is an opportunity to see acquisitions reduce the number of players,” says Greg Hosch, CEO, Harris Cos.

Ted Lynch, CEO of Southland Industries, says the industry is seeing the beginnings of another series of rollups, as larger firms begin to acquire smaller firms. “There are a lot of smaller firms that are having second thoughts about continuing to go it alone and are considering selling to stay viable,” he says.

Limbach is another firm on the acquisition trail. After going public this time last year, it has been searching for suitable candidates for acquisition. “We just hired a new executive vice president in charge of mergers and acquisitions,” notes Bacon.

Bacon says Limbach’s dedicated design group provides a full range of design services. But the rm is now actively scouting electrical contractors for acquisition to go along with its mechanical work. This strategy will help Limbach to provide the full MEP package on design-build and integrated-project-delivery jobs, says Bacon.

Southland Industries is another mechanical contractor that has a dedicated design group to provide a full MEP design package to projects. Lynch says Southland always is looking for potential acquisitions. But unlike Limbach, Southland is not actively pursuing electrical contracting capabilities. “We have a lot of great electrical contractor partners and are not looking to replace them with in-house capacity,” he says.

Limbach and Southland are not alone in expanding their capabilities beyond their core. Power Design recently expanded to include a mechanical division, hiring a team of mechanical engineers to learn its business model and start taking on projects. “This is a big step for us as an electrical subcontractor because now we can offer even more of a holistic solution to our customers by bringing in the mechanical engineering piece,” says Lauren Permuy, vice president of business development. “It gives us more of a competitive edge against other electrical contractors and engineers, and we look forward to seeing the division grow.”

Collaborative Environment

These moves into a wider range of contracting and design is a reflection of general contractors’ and owners’ increasing demands on subcontractors and specialty contractors to provide more services, sooner. For example, Austin notes that, “in anticipation of our industries’ growing emphasis on turnkey projects, Quanta developed a full range of planning, engineering, procurement and construction capabilities.” He says Quanta’s integrated, self-perform model allows it to meet electric power and oil-and-gas infrastructure demands.

Design-build and integrated project delivery increasingly are demanding early subcontractor input. In fact, major subcontractors now are being seen more as partners than as hired hands. “In these projects, a core team of the general contractor, architect and major key subcontractors, such as mechanical and electrical, assemble early to set the project’s goals and establish shared norms for the project,” says Ash Awad, chief market of cer for McKinstry.

As complexity in the building envelope increases, project teams are seeking earlier involvement from many different trades to assist in constructibility-driven design decision-making and accurate budget pricing. “What has emerged is an extensive design-assist period that integrates intense specialty-contractor involvement in helping the owners, construction managers and general contractors mitigate cost and schedule risks,” says Jeffrey Vaglio, director of the advanced technology studio at Enclos.

Technology is helping subcontractors to participate early in the construction process. “The use of three dimensional computer-based design is revolutionizing our industry. This technology is enabling true collaboration in the preconstruction phase and aiding in the delivery of information to the workface,” says Goodrich of Gaylor Electric.

Technology is helping subcontractors to participate early in the construction process. “The use of three dimensional computer-based design is revolutionizing our industry. This technology is enabling true collaboration in the preconstruction phase and aiding in the delivery of information to the workface,” says Goodrich of Gaylor Electric.

Risky Business

While subcontractors are giving more input into the construction process, many complain that some owners and GCs continue to impose tough contract conditions. Contracts are becoming more onerous, requiring longer legal reviews and costs. “Gone are the days of a handshake and signature. Many contracts require quite a bit of back-and-forth for weeks or even months before getting someone on board,” says Michael Haber, managing partner of W&W Glass.

These contract clauses are causing more interactions not over the project but over what is expected and what is required. “Relations are good. However, the consistent additional risk we, as a large subcontractor, are being asked to assume means additional discussion on both ends regarding terms and conditions,” says Jeff Heymann, vice president of Benson Industries Inc.

The increased risk-shifting may jeopardize contractors that are not used to assuming such liability. Newtron Group President John Schempf says, “We expect that some contractors will struggle financially to compete with contractors that have regularly accepted risk in the past.”

Subcontractors also worry about other contract terms. At the project level, “we have seen a shift in overall management responsibilities that owners put on demolition contractors,” says David H. Grif n Jr., president of D.H. Grif n Cos. The industry is shifting toward a “design and deconstruct” model, with owners requesting complete technical and strategic plans at the beginning of the bidding process, particularly in the power industry, he says.

The increasing use of so-called owner-controlled insurance programs (OCIPs) and contractor-controlled insurance programs (CCIPs) is a cause of concern, too. “The problem arises when the OCIP or CCIP insurance doesn’t provide the same coverage your own insurance normally provides, both in coverage and deductibles,” says Richard Pennington, executive vice president of Dorvin D. Leis Co.

A perennial problem for subcontractors is getting fully paid in a timely manner. A sign of this problem is found in the results of the Top 600 survey. Over the past three years, the average percentage of late payments and the average number of days late have remained consistent. In fact, the average number of days late has increased to 37.2 in 2017 from 35.6 in 2015.

“These payment delays affect the industry as a whole, higher prices to cover lost interest and earnings, lawsuits for damages and delays in timely payments. Quick pay must be the hot topic going forward,” says Jim Verner, president of Acousti Engineering Co. of Florida.

For many subcontractors, payment transparency is critical. “Most contracts around the country have pay-when-paid clauses,” says Nelson of ASA. But subs often don’t know when the GC is paid, so they don’t know when they should expect their own payment. She notes that some cities, such as San Antonio and the District of Columbia, already publish on their websites their disbursements to contractors, giving subs a heads-up on when their progress payments should be expected.

Now, the state of California Legislature has passed a statewide requirement that mandates all state agencies to publish in the state contracts reg- ister notice of progress payments made to prime contractors within 10 days of payment. And Con- gress has proposed a federal Small Business Act amendment that would impose similar requirements on federal agencies for progress payments on federal projects.

Staff Shortages

Staff Shortages

Staff Shortages

Staff ShortagesPerhaps the biggest issue among subcontractors is the growing staff shortages around the country. “Young people just aren’t seeking out skilled training at the rate that they’re seeking out college degrees, despite the good wages and challenging work,” says John Boncher, president and CEO of Cupertino Electric Inc. He says Cupertino has been educating students and their parents about what a career in the skilled trades can offer. “We need to update our approach, embrace social media and getting this next generation excited about a future in the construction industry.”

Many firms worry that the Trump administration’s continuing efforts to limit immigration may hurt the industry. “What hurts is the clamping down on work- ers from other countries and the policy of not allowing guest workers,” says Permuy. “This will continue to negatively impact costs to the industry.”

Retaining qualified people is a key to success. Guzzi of Emcor says workers are looking to firms that will provide basic security. He says workers are asking, “Are you going to pay me at the end of every week, and are you going to make sure the jobsite is safe? Do you have supervisors who will provide leadership? And if I do a good job, can I expect to become a regular member of the team?” Keeping these issues in mind during the downturn and throughout the long recovery, Emcor has worked hard to answer yes to all these questions.

However, Nelson of ASA points out that, if the industry goes into recession in the next year or two, the loss of workers could have a devastating long-term impact on the industry workforce. “The baby-boom generation, who continued to come back time and again after cutbacks in previous industry recessions, may decide to hang it up if they are laid off or end up being put on short hours during the next recession,” she says. Further, Nelson points out that the younger generation of workers who haven’t experienced the cyclical nature of the industry may decide they are better off in other industries, rather than holding on or returning to construction after their first down cycle rebounds, leaving the industry’s staffing crisis even more severe.

However, Nelson of ASA points out that, if the industry goes into recession in the next year or two, the loss of workers could have a devastating long-term impact on the industry workforce. “The baby-boom generation, who continued to come back time and again after cutbacks in previous industry recessions, may decide to hang it up if they are laid off or end up being put on short hours during the next recession,” she says. Further, Nelson points out that the younger generation of workers who haven’t experienced the cyclical nature of the industry may decide they are better off in other industries, rather than holding on or returning to construction after their first down cycle rebounds, leaving the industry’s staffing crisis even more severe.

One plus in the recruitment of young people is the recent Trump administration move to expand apprenticeship programs. Goodrich of Gaylor Electric believes this action will be a big boost to the industry. “Approving high-quality, industry-recognized apprenticeship programs will go a long way toward bridging the skills gap and training the construction workforce we need today and tomorrow,” he says. Across the country in 1,400 locations, ABC has built a network of chapters and affiliated training centers that offer more than 800 apprenticeship, craft, safety and management training programs to build the people who build America, he says.

A legal issue for subcontractors is workers’ compensation. Nelson says there are concerns that an aging workforce may increase the number of on-site accidents, putting pressure on workers’-comp rates.

Some contractors say there is not enough policing of questionable workers’-comp claims. “We would like to see more attention given to fitness for duty as a way to mitigate this situation,” says Victor E. Salerno, CEO of O’Connell Electric Co. Inc.

However, a Texas trial court’s recent workers’- compensation ruling has many in the industry and insurance watching carefully. It concerns “exclusive remedy” provisions in workers’-comp laws, barring injured workers from suing their employers if the employer is covered by state-authorized workers’-comp insurance.

Texas A&M University awarded a $4.5-million contract to expand and renovate Kyle Field on the campus at College Station. The job was covered by an OCIP, including a workers’-comp policy that covered the GC and major subcontractors.

A worker was killed on the job, and his family sued the GC and several subcontractors for wrongful death. Despite a Texas law that says workers’ comp is the ex- clusive remedy for worker injuries and deaths, a Texas trial court ruled in Manhattan | Vaughn, JVP v. Garcia that, since neither the GC nor the subs were the direct purchaser of the workers’-comp insurance and were only OCIP subscribers, workers’ comp was not the exclusive remedy for a worker’s death. The court upheld the jury’s $53.8-million wrongful-death verdict.

ASA and other organizations are working to overturn this ruling. Nelson of ASA says the decision conflicts with other rulings on the issue in Texas and elsewhere and hopes the Houston court of appeals will reverse it. Still, this is “a scary scenario” if other courts start looking at this case for guidance, she says.